Every payment company wants stablecoins. Almost none can ship them. Here's what the data actually shows, and what it takes to go from evaluation to live.

In this article

- The demand signal is unambiguous

- Why most companies can't ship it

- The four real barriers to integration

- How to actually accept crypto payments

- Which assets and chains to support

- Compliance: the layer most teams underestimate

- What merchants need to know

The conversation has shifted. Accepting crypto and stablecoin payments is no longer a question of whether the technology works, it does. In 2025, annualized onchain stablecoin transaction volume surpassed $46 trillion, now rivaling the throughput of major card networks. Visa and Mastercard now support USDC settlement, allowing card obligations to be discharged onchain. JPMorgan has a deposit token live on Base. Stripe charges a flat 1.5% for stablecoin processing. The rails are real, and they're in production.

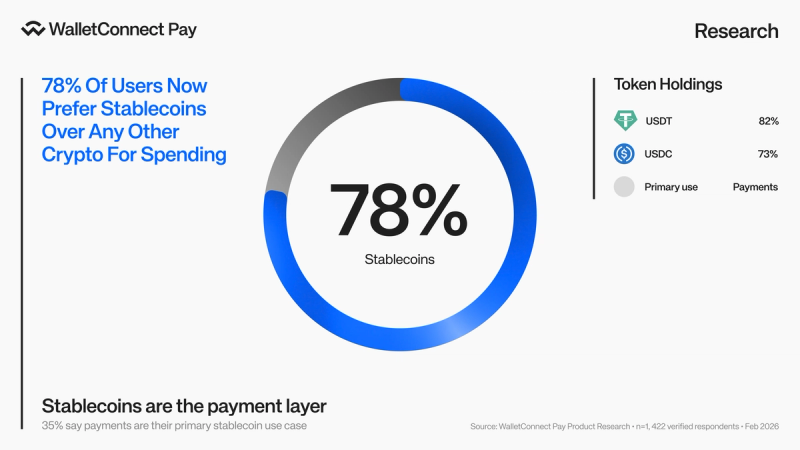

More importantly, the users are ready. WalletConnect's survey of 1,127 active crypto users across 10 regions found that 96% want to pay with crypto but can't find enough places to do it. A BVNK study found that 42% of stablecoin holders want to spend on major purchases, while only 28% actually do so today, not because they lack funds or intent, but because merchant acceptance is still the bottleneck.

The demand-side case is closed. The question now is entirely on the supply side: how does a payment company actually go live with crypto and stablecoin payments?

Why most companies can't ship it

The gap between "we want to do stablecoins" and "stablecoins are live in production" is wider than most teams expect, and it's almost never a technology problem. 86% of financial firms report their infrastructure is ready for stablecoin adoption, shifting the focus from pilots to execution.

The real obstacles are operational: compliance integration, settlement reconciliation, multi-chain complexity, and the expertise gap inside traditional payment teams. Most companies need multiple vendors to support fiat and stablecoin rails, then stitch everything together themselves, creating two providers, two reconciliation streams, and twice the failure modes.

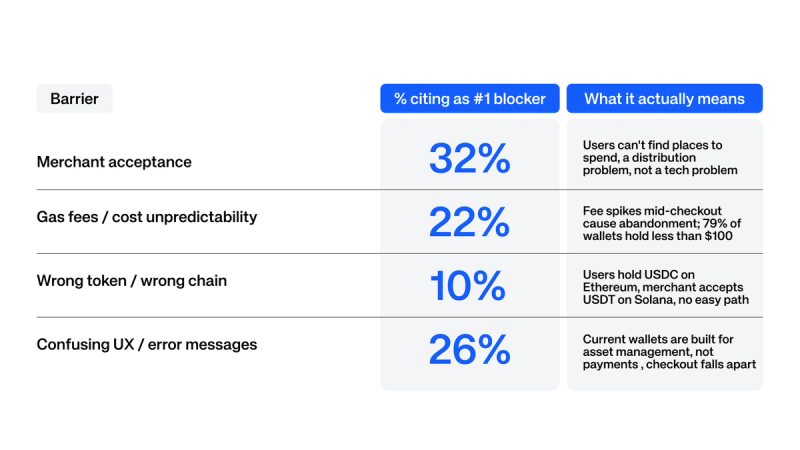

WalletConnect's network data tells a specific version of this story. Across 22 PSPs and 201 countries, we processed $3.26 billion in payment volume for the last quarter of 2025, but that same network shows exactly where the drop-off happens. 76% of active crypto users abandoned a payment in the past six months. The causes: gas fees higher than expected (45%), transactions taking too long (30%), confusing error messages (26%), wrong token on wrong chain (18%).

WalletConnect Network Data: 839,813 completed transactions from 460,550 unique sessions across 22 PSPs, 177 wallet providers, 125 chains, and 201 countries, Feb 2025 to Jan 2026.

These aren't edge cases. They're the standard experience when crypto payments are integrated without solving the underlying complexity. The companies that go live successfully are the ones who treat this as an orchestration problem, not a plug-in problem.

The four real barriers to integration

Based on WalletConnect's data across 22 live PSP integrations, the blockers that delay or derail stablecoin payment launches cluster into four categories:

The common thread: none of these is insurmountable. They're each a solvable infrastructure problem, gas abstraction, token routing, chain abstraction, standardised checkout flows. The difference between PSPs that ship and PSPs that stall is whether they try to solve these themselves or use the infrastructure that already exists.

There are three routes to accepting crypto and stablecoin payments. Each has a different time-to-market, cost structure, and level of ongoing complexity.

Option 1: Build in-house

Building your own crypto payment stack means managing wallet connectivity, chain integrations, settlement logic, compliance workflows, and reconciliation, all from scratch. For most PSPs, this means 6–18 months of development, a dedicated blockchain engineering team, and ongoing maintenance across every chain you support. Bank sponsorships alone typically require 6 to 12 months of onboarding before a single transaction clears. It gives you full control. But control isn't the same as speed, and speed is what the market is pricing right now.

Option 2: Use a crypto payment gateway or a standalone provider

Institutions evaluating stablecoin payment rails in 2026 prioritise reliability above all: security and compliance, instant settlement, multi-chain coverage, and developer-grade APIs. Each is a separate integration from your existing payments stack. You end up with parallel rails, separate reconciliation, and two systems to maintain.

Option 3: Integrate through existing payment infrastructure

The most efficient path, and increasingly the standard one, is embedding stablecoin acceptance into existing payment flows rather than running it in parallel. Shopify's USDC integration is embedded inside Shopify Payments, meaning merchants turn it on alongside credit cards without adding new providers or changing workflows. That's the model: stablecoins as an option in the existing checkout, not a separate product the merchant has to manage.

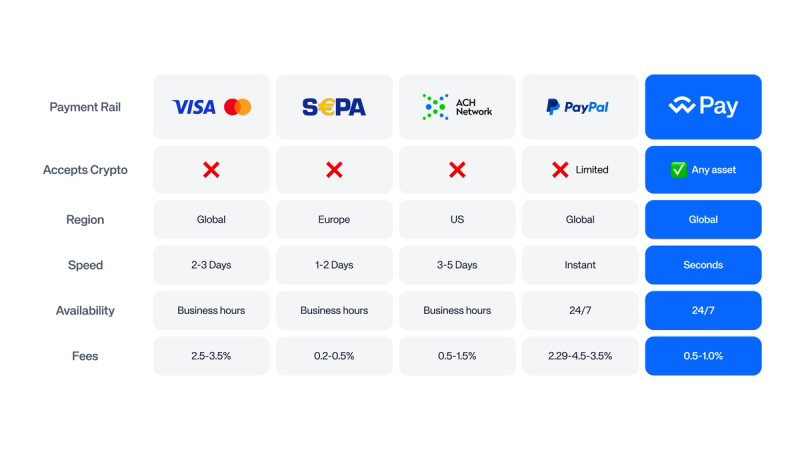

WalletConnect Pay is built on this principle. A single integration gives PSPs access to 500 million+ wallets across 125+ chains and 700+ wallet providers, with compliance, routing, and settlement handled at the infrastructure layer. No rebuild of existing stack required.

The fastest path to live is infrastructure that plugs into existing settlement and reconciliation flows rather than creating a parallel system. Every additional integration point is a failure mode and a maintenance cost.

Which assets and chains to support

One of the most common mistakes in crypto payment integration is starting with too narrow an asset and chain strategy, and then discovering mid-launch that your users' holdings don't match what you accept.

WalletConnect's onchain analysis of 1.11 million wallets reveals the complexity: users hold stablecoins across an average of 2.82 chains and 2.65 different tokens per wallet. 107 distinct stablecoin symbols appeared in our ecosystem over 12 months. The global picture at chain level: BNB Chain leads by holder count globally with 574,000 holders, while Ethereum holds 65% of all stablecoin value. Users park value on Ethereum, prefer to pay on Base, and hold the broadest token diversity on BNB Chain.

The practical implication: accepting only USDC on Ethereum will work for a slice of your user base. Supporting USDT and USDC across Ethereum, Solana, Base, BNB Chain, and Tron covers the overwhelming majority. Start narrow if you need to, but build for expansion from day one. Infrastructure that requires a new integration per chain will bottleneck you quickly.

Beyond stablecoins: accepting Bitcoin and Ethereum matters more than it used to. WalletConnect Pay supports any asset on any chain, because users hold what they hold. Restricting to stablecoins-only turns away users with BTC or ETH who would otherwise pay. In North America specifically, 29% of crypto users prefer paying with BTC or ETH directly over stablecoins.

The single biggest difference between a P2P crypto transfer and a compliant payment flow is everything that surrounds the transaction. The blockchain handles value transfer in seconds. Payments require everything around it, and the gap is operational, not technical.

Four things need to be in place before you can call a stablecoin payment integration production-ready:

- 1 KYC / AML at transaction time Compliance screening needs to happen in real time, not as an afterthought. The regulatory frameworks now exist — GENIUS Act in the US, MiCA in Europe, DTSP in Singapore — but operationalising them within live payment flows is an engineering and process challenge that most teams underestimate. Plan 6–12 months of runway to get compliance infrastructure production-ready for cross-border flows.

- 2 Travel rule compliance Cross-border stablecoin payments trigger travel rule requirements in most major jurisdictions. This means transmitting originator and beneficiary information alongside the transaction. It's now table stakes, not optional — and it requires infrastructure that handles it automatically at scale.

- 3 Settlement and reconciliation PSPs need deterministic settlement with reconciliation flows that map to existing accounting systems. Crypto transactions settle onchain, but downstream processes — invoice matching, reporting, ERP integration — require structured data that most blockchain transactions don't natively provide. Solve this before launch, not after.

- 4 Dispute resolution and refunds Card networks have decades of chargeback infrastructure. On-chain payments have no equivalent. Merchants need a defined path to handle disputes, process refunds, and manage customer service flows. This is a product and process requirement — build the refund workflow before you accept the first payment.

The companies that will have a first-mover advantage in 2026 are the ones that invested in compliance infrastructure during the uncertainty period. The regulatory clarity that makes this easier also means the window for "we're still figuring it out" is closing fast.

If you're a merchant rather than a PSP, the picture is simpler, and more commercial.

More than half of crypto holders have bought something specifically because a merchant accepted stablecoins, rising to 60% in emerging markets. Accepting crypto payments is a customer acquisition lever, not just a payment method choice. The customers who pay with crypto spend 15–25% more on average. They actively choose merchants who accept it.

The economics for merchants are straightforward:

For merchants, the integration path runs through your PSP. If they support stablecoin payments, you inherit that support through your existing relationship. For in-store, QR-based checkout via POS is the current standard: the customer scans, approves in their wallet, and the transaction settles onchain. No new hardware required.

The choice merchants actually face isn't "should we accept crypto", it's which assets and which chains to support. Start with USDC and USDT. Add Bitcoin and Ethereum if your customer base skews toward holders. Let your PSP handle the rest.

Before going live with stablecoin payment acceptance, work through this list. Every unchecked item is a potential failure mode at checkout.

- Define your asset and chain scope Which tokens will you accept? On which chains? USDC + USDT across Ethereum, Base, Solana, and BNB Chain covers the majority of WalletConnect network volume. Avoid single-chain-only launches if you can.

- Choose your integration approach Build, standalone gateway, or embedded via existing PSP infrastructure. The third option is fastest to market and lowest ongoing maintenance. Understand what your existing PSP supports before building anything.

- Solve gas abstraction before launch 45% of payment abandonment is caused by gas fees higher than expected. Users should not see gas fees at checkout. Use paymaster architecture or a network that handles this at the infrastructure layer.

- Build compliance in, not on top KYC/AML, travel rule, sanctions screening — these need to be native to the payment flow, not a manual review queue. If your integration partner handles this, confirm exactly how and at what transaction size thresholds.

- Map settlement to existing reconciliation Onchain settlement is near-instant. Your accounting and ERP systems need structured data that maps to existing invoice and reporting flows. Confirm your provider outputs this before you commit to the integration.

- Define your refund and dispute path Blockchain transactions are irreversible. You need a defined process for refunds, typically a new outgoing transaction to the customer's wallet. Build this workflow and document it in your terms before accepting the first payment.

- Test across wallet types WalletConnect data shows significant variation in payment completion rates by wallet. Coinbase Wallet users complete 26% of attempts without abandonment; Trust Wallet and Rainbow users only 14%. Test your checkout across MetaMask, Binance Wallet, Zerion.

Accepting crypto and stablecoin payments is no longer a speculative product decision. The user demand is documented. The institutional validation is real. The regulatory frameworks are in place. The stablecoin market is now large enough to influence financial infrastructure discussions rather than sit outside them.

What hasn't caught up is execution. The PSPs and merchants who close the gap between "we're evaluating" and "we're live" in 2026 will define the payment experience for the users who come after, a cohort that spends more, converts better, and actively chooses the merchants and platforms that meet them where they already hold value.

The infrastructure is ready. The question is whether your organisation is.

Every problem this guide describes, fragmentation across chains and tokens, gas abstraction, compliance integration, reconciliation, and wallet compatibility, is what WalletConnect Pay was built to solve. It's live in production today across 22 PSPs, 177 wallet providers, and 201 countries, having processed $3.26 billion in payment volume in Q4 2025. If you're a PSP ready to move from evaluation to live, or a merchant looking to accept stablecoins and crypto without rebuilding your stack, WalletConnect Pay is available now, a single integration, any chain, any asset, built for the payments industry rather than the crypto industry.